Over the last few months we're had several important signs that the economy may be bottoming.

The Conference Board has recently reported that leading indicators spiked up last month and consumer confidence has improved. In addition, the number of people who say the country is on the right track has been increasing since October, while the number of people who say the economy is getting better is increasing. We've possibly seen a bottom in retail sales and durable goods orders. Finally, it appears that the four-week moving average of initial jobless claims as topped out. While all of this is preliminary data which could change given the volatile nature of the economy, things do appear to be moving forward. That means we need to start looking at what kind of recovery we'll see. And in that category there is a great deal of concern about what will actually drive growth.

To illustrate this issue, let's break US GDP down into its four components. Personal consumption expenditures, gross private domestic investment, exports and government spending.

Personal consumption expenditures account for 70% of US economic growth. Unfortunately, the US consumer does not appear ready to lead the economy out of recession. The main issue is US households are heavily indebted:

U.S. household leverage, as measured by the ratio of debt to personal disposable income, increased modestly from 55% in 1960 to 65% by the mid-1980s. Then, over the next two decades, leverage proceeded to more than double, reaching an all-time high of 133% in 2007. That dramatic rise in debt was accompanied by a steady decline in the personal saving rate. The combination of higher debt and lower saving enabled personal consumption expenditures to grow faster than disposable income, providing a significant boost to U.S. economic growth over the period.

In the long-run, however, consumption cannot grow faster than income because there is an upper limit to how much debt households can service, based on their incomes. For many U.S. households, current debt levels appear too high, as evidenced by the sharp rise in delinquencies and foreclosures in recent years. To achieve a sustainable level of debt relative to income, households may need to undergo a prolonged period of deleveraging, whereby debt is reduced and saving is increased.

Here is the accompanying chart:

Simply put, US households have gone on a debt acquisition binge over the last 30 years. The primary event forcing them to deleverage is the massive loss of assets over the last few years thanks to the stock and housing market corrections. According to the Federal Reserve, household wealth has decreased from $64.361 trillion in 2Q07 to $51.476 trillion in 4Q08, or a decrease of 20%. This decrease means households have fewer assets relative to debt, meaning households are in fact poorer. This in turn forces consumers to pay down debt at the expense of spending. In summation, there is little reason to think that consumers will return in droves to the malls. It is far more likely they will consume less, leading to a slower recovery.

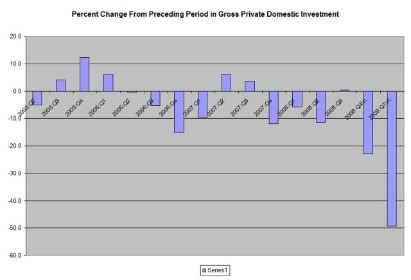

Next, there is investment. Here is a chart of the percentage change from the preceding quarter in gross private domestic investment.

Notice how this number has been negative for nine of the last 12 quarters. In other words, the US economy is already in an investment recession. And there is little reason to think we'll be coming out of it anytime soon.

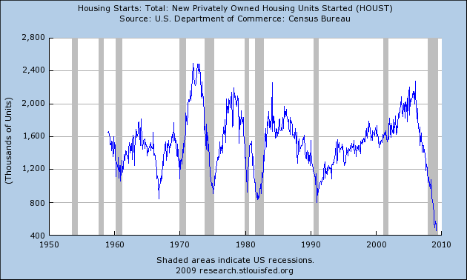

Housing starts are already at 40 year lows.

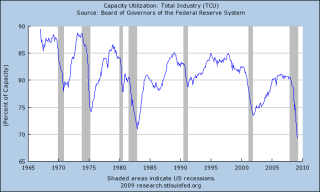

Capacity utilization is also at 40 year lows, meaning there is little incentive for companies to buy new capital equipment.

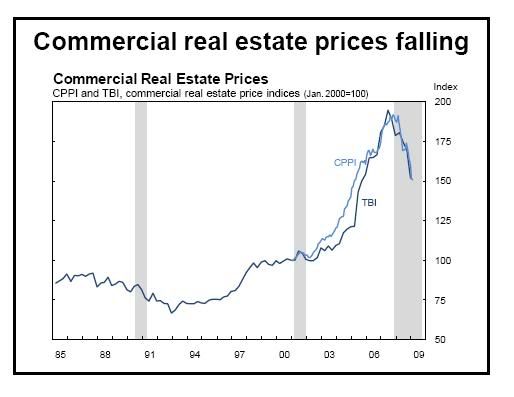

Commercial real estate prices are falling as well, indicating a lack of demand and therefore no need to build more commercial property.

In short, there is no reason to think investment will bring us out of the recession either.'

Then we have exports. First, remember the US is is a net importer and has been for several decades. That means exports haven't bee a positive contributor to GDP for some time. But most of out trading partners are also in a recession so they have no need to buy things from the US. In other words, don't expect exports to bring us out of the recession either.

Simply put, there are no parts of the economy ready to step up to the plate and take the lead pulling the US out of recession. As a result:

Americans may have to get used to unemployment greater than 8 percent for the first time since 1983 and an economy that won’t grow much beyond 2 percent as a consequence of the lost confidence in consumer credit that shattered financial markets.

By this time next year, "the market will realize that potential growth for the U.S. is no longer 3 percent, but is 2 percent or under," Mohamed El-Erian, chief executive officer of Pacific Investment Management Co., said in an interview with Bloomberg Radio.